Introduction

The cost impact to the U.S. healthcare system by the COVID-19 pandemic has been estimated by reputable studies in a range of 6%-15% of U.S. healthcare spend in 2020. These studies are of special interest to self-insured employers, health plans, and reinsurers for pricing and planning purposes. An important feature of these models is that they do not attempt to quantify the behavioral changes of beneficiaries who are unable or unwilling to seek care during times of social distancing and hospital resource scarcity.

EPIC calculates that in 2020, COVID costs for the U.S. will represent an unanticipated spend increase of 8%, but when offset by the reduction in cost for behavioral changes, it will total 15%. EPIC is making its model available to self-insured employer clients, whose projected spend will vary by healthcare product, geography, population demographics, and the impact of their stop-loss reinsurance program. EPIC’s model is the first to offer self-insured employers an estimate of the cost impact based on policy effective date and stop-loss retention.

DOWNLOADABLE RESOURCES

Pandemic Magnitude and Timing

Estimates of healthcare costs over the course of the pandemic are highly dependent on it’s trajectory, which is itself highly dependent on myriad factors around personal behavior, institutional response, scientific and logistical advances in testing and treatment. The most commonly cited model, from the Institute for Health Metrics and Evaluation, estimates 135,000 deaths through August 4th. A survey of experts conducted by the University of Massachusetts at Amherst supports this model estimate.

Survey estimates of smallest, most likely, and largest number of deaths in the U.S. by the end of 2020 (millions)

Each bar represents one expert’s estimated range. Yellow dot represents the expert’s most likely estimate.

A short-term estimate of deaths for the Spring of 2020 is critical to support decision-makers but is not ideal for estimating the costs across the length of the pandemic. Global pandemics of this magnitude are nearly unprecedented, but all evidence shows that this pandemic will persist beyond August or re-appear at some point in the future.

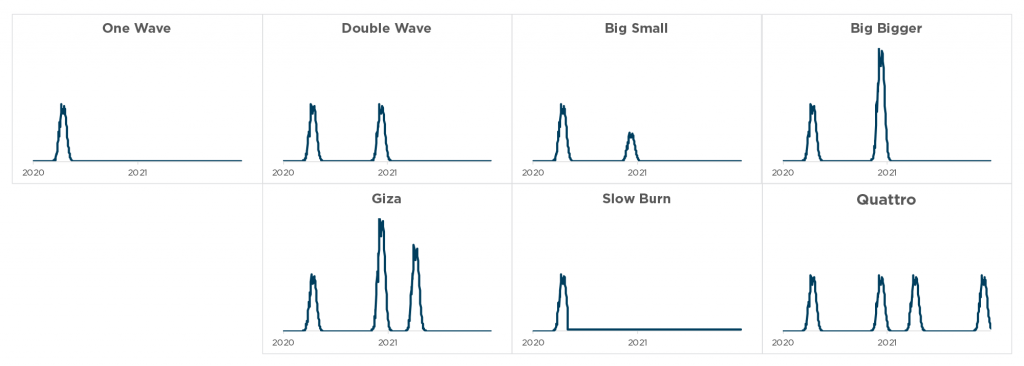

U.S. Deaths per Day

EPIC’s approach is to also model scenarios with one or more additional ‘waves’ of the disease that might recur over the course of 2020 and 2021.

The timing of these waves is key to our approach, because it enables us to estimate the timing and magnitude of delayed care, which coincides with and anticipates periods of social distancing and hospital resource scarcity. The delayed-care model also estimates the rate of filling of care backlogs during periods of low infection rates.

EPIC Hospitalization and Relative Care Delay

Delay of Care

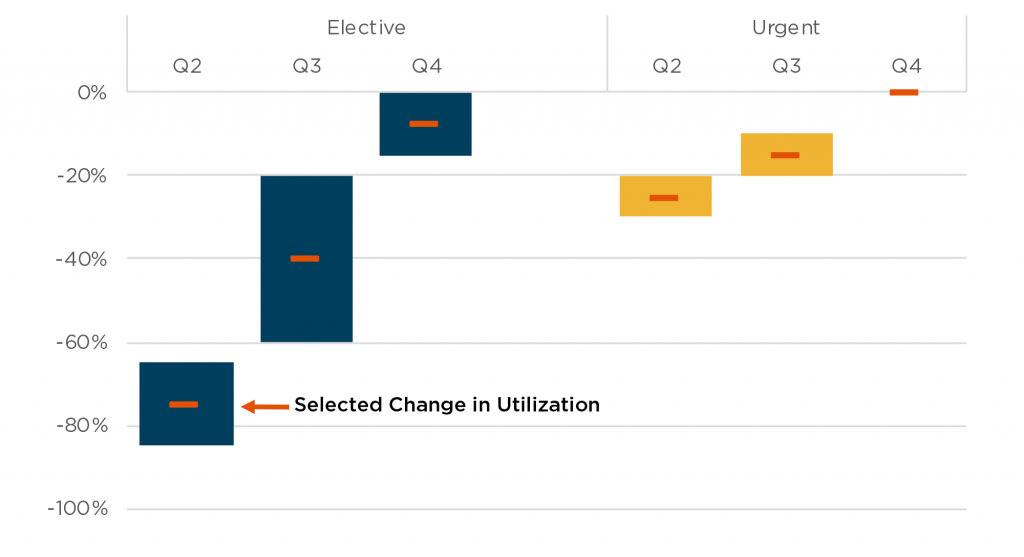

Early learnings from outbreaks in the U.S. indicate that elective procedures are being postponed, and in some cases indefinitely deferred. Some states loosened restrictions on elective surgeries in late April, and other states followed in May. Perhaps more surprising is how many patients are prioritizing social distancing over the still-available non-elective procedures and emergency care. We believe that for some populations the cost offsets of this delay and deferral of care are of a magnitude that may exceed the direct costs of testing and treatment.

Change in Utilization by Service Type

Source: Johnson & Johnson investor page webcast of Q1 results

In advance of claims data becoming available for March and April in hard-hit areas, an examination of the unwillingness of patients to present at hospitals paints the picture that care deferral will be higher than analysts expect for urgent care. Consider cardiac care in places where there is uninterrupted availability of resource:

- In Spain, diagnostic tests were reduced by 57% in cardiology departments. PCI in STEMI was down by 40% Source: Impacto de la pandemia de COVID-19 sobre la actividad asistencial en cardiología intervencionista en España

- In Hong Kong, cardiac patients who eventually underwent PCI in STEMI took 4 times as long after symptom onset to present at the hospital than prior to the pandemic. Source: Circ Cardiovasc Qual Outcomes. 2020;13:e006631. DOI: 10.1161/CIRCOUTCOMES.120.006631

- In the first week of April, cardiac arrest calls were up 300% over the same period in the prior year. The number of non-revivable cardiac arrest calls were up over 700% from the same period in 2019. Source: FDNY

- An informal survey of cardiologists by Angioplasty.org indicated that STEMI/ACS admissions were down by about 50% in early April.

In early April, New York City reported a staggering increase in the number of at-home deaths, an increase from 25 per day to 280 per day. Some of these patients will have been undiagnosed COVID-19 deaths, others resulted from the stressors of the pandemic and social distancing. We believe a significant remaining portion represent patients whose health would be restored or lives prolonged through high-cost inpatient care.

Anecdotal reports indicate similar reductions in hospital admissions for other acute conditions like appendicitis. If serious, painful, sudden conditions for which patients know there are known, effective treatments are being ignored, it will have serious implications on health and mortality in the short term and may persist beyond the period of social distancing.

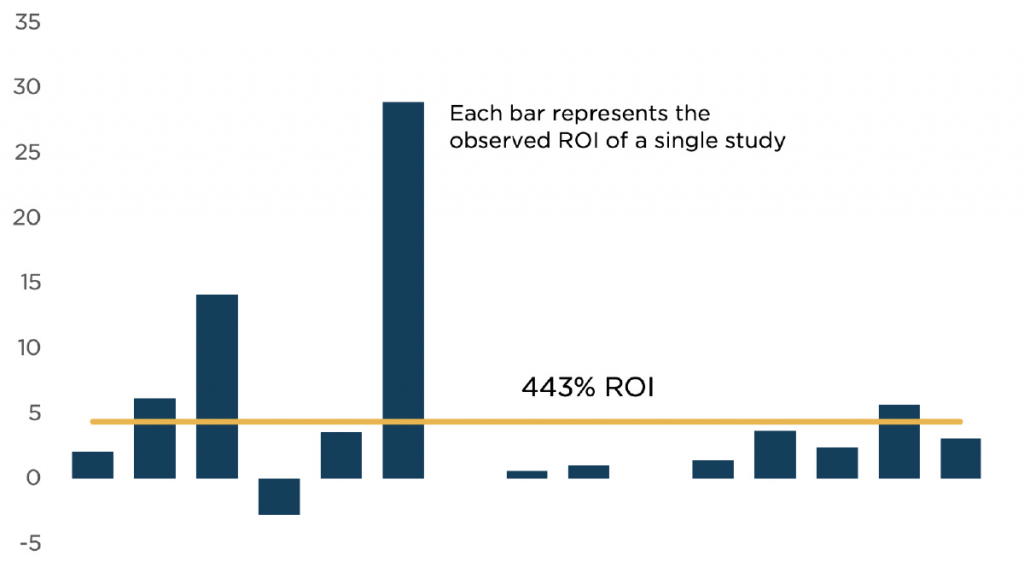

Disease Management

We expect that some portion of the deferred care should be considered preventive and disease management. In the same sense that disease management is thought to have a net-negative cost over the long term, we expect that the absence of disease management will lead to short-term cost savings, but higher disease costs in later 2020 and beyond. This will represent a shift of costs from earlier claims to later, but also from retained claims to higher-cost reinsured claims. A metastudy of congestive heart failure cases demonstrated a significant reduction in health care costs from investment in disease management.

Disease Management ROI Congestive Heart Failure

Source: Goetzel RZ, Ozminkowski RJ, Villagra VG, Duffy J. Return on investment in disease management: a review. Health Care Financing Review. 2005;26(4):1–19.

Permanently Delayed Care

Much of the expected health care that is not being realized during the pandemic, like knee replacement surgery, will be performed in the time after or between waves of the pandemic. Other care will not return, like a missed prescription fill or a regular behavioral health appointment. The care will be limited by availability of providers to deal with the backlog and the elimination of the medical concern through natural recovery or mortality. It is difficult to estimate how much of the backlog of care will be addressed, but most estimates indicate that less than 50% of the backlog will ultimately be filled.

In response to the unprecedented challenge of COVID-19, the U.S. healthcare system has rapidly expanded its critical care capacity and access to telemedicine. Access to testing and treatment has been improved by cost shifting from consumer to payers. Non-traditional participants in the delivery of medicine, including charities, the armed forces, retired healthcare professionals, federal resources, interstate compacts, and donors of medical equipment have bolstered the U.S. arsenal to fight the pandemic by caring for COVID-19 and other patients. This will offset expected COVID claims cost and also may have a similar financial impact to payers as permanently delayed care.

Cost of COVID Testing

Testing costs are well understood on a unit-cost basis, but will change as the health system’s focus shifts away from expanding critical care capacity to controlling the community infection rate. Initial testing was focused on highly symptomatic patients and is shifting towards monitoring high-contact first-responders, teachers, grocers, and public health officials. Mildly symptomatic patients, many of whom eventually become highly symptomatic, will increasingly have access to test results.

Serology tests that identify whether a patient has had the coronavirus in the past may not demonstrate immunity from the pandemic but are likely to be used as a litmus test of whether individuals are safe enough to relax social distancing. There will likely be more consumer demand for these tests, a vaccine, or prophylactic drug regiments than supply, at least initially. As part of a coordinated societal response to the pandemic, this category of testing and treatment is likely to be rationed by and financed through public entities and not traditional payers.

Although some employers may seek to distribute antigen testing and prophylactic treatment outside of the health plan benefit, we exclude the costs of these regiments from self-insured employers and health plan payers.

Direct Cost of COVID Treatment

Most models of the costs of coronavirus or flu pandemic are based on the historical cost of an episode of inpatient pneumonia, which bears many similarities in terms of inpatient treatment costs, including length of stay, use of ventilators and use of high-cost ICU beds. The cost of this common condition is well understood.

EPIC’s model calculates separate costs by member in consideration of their presumed length of stay, and disease severity, with higher costs for the use of ICU and/or ventilator. Unlike EPIC’s model, we believe the pneumonia paradigm may understate the costs of care for a policy period because the starting point is an episode of care as opposed to a longitudinal view of the costs of care. For example, acute kidney injury (AKI), a common co-morbidity for pneumonia and COVID-19 patients, often results in high costs in the short-term. Politico reports that approximately 20% of COVID-19 patients in New York City hospitals require dialysis often for days or weeks after pneumonia passes and they are weaned off ventilators. This unexpected development has led to shortages of the dialysis fluids and trained nursing staff, even as the city managed to avert its initially anticipated shortage of ventilators.

Despite recovery from AKI, the lasting impact of the episode may lead to development of serious and high-cost chronic kidney disease, including end stage renal disease. Patients with chronic kidney disease are extraordinarily expensive to treat, likely costing the U.S. healthcare system more than the costs of treating all cancer patients combined.

In addition to renal disease, we estimate other costs associated with COVID-19 that are not considered in summary information about a pneumonia episode. These costs, including the use of extracorporeal membrane oxygenation (ECMO), cardiovascular complications, and healthcare acquired infections like sepsis, do not vastly increase the costs of COVID treatment in the aggregate, but are of special concern for stop-loss reinsurers, as these complications often result in annual claims of greater than $1 million per beneficiary per year.

Cost Related to COVID-19 Complications As a percentage of direct COVID-19 Cost

Drugs and Alternative Treatment

As of the date of this writing, COVID-19 remains a disease with no known effective treatment. Around the world, trials and experimentation are underway, mostly to test antiviral drug therapies that are known to be effective against other diseases. We expect that any treatment shown to be highly effective would come at a moderate price tag, as the authorities would leverage or use the Defense Production Act to weaken patent protection and/or encourage mass production of manufacture of the drugs.

We expect that if either of the two most widely tested therapeutics, hydroxychloroquine or remdesivir, were established as the standard of care for COVID-19 patients, the full course of therapy would cost payers less than the swab test to determine whether a patient had been infected by the virus. As such we don’t explicitly take account of these therapies in our model.

Cost Sharing

Most private insurers are required or have voluntarily waived cost sharing for testing and doctor visit relating to the diagnosis of COVID-19. There is generally no requirement for private insurer to waive cost sharing for treatment of COVID-19. Cost sharing for traditional Medicare and Medicare advantage beneficiaries is also waived for testing and diagnosis. Traditional Medicare beneficiaries, however, are subject to cost sharing related to treatment. The cost sharing for treatment under Medicare Advantage will vary by plan, with some plans possible waiving some cost sharing for treatment.

Our model estimates assume that cost-sharing by beneficiaries is unchanged by the pandemic. In some cases, the deductible would be maximized even in the absence of COVID claims. In other cases, the health plan will not apply deductibles and co-pays. Explicit accounting for the changes in cost-sharing would not have a material impact on our net cost estimates.

Workers’ Compensation

The most at-risk employer populations are at-risk of contracting COVID-19 both at home and at work. Workers’ Compensation insurance will act as a primary payer with respect to health claims when an investigation indicates that an accident or occupational disease arises out of employment. In some cases, this type of investigation is not feasible, and so state Workers Compensation boards are likely to presume workplace exposure in the absence of evidence to the contrary. Highly exposed industries including first-responders, retail employees, and healthcare professionals would then see a shift from health insurance claims to Workers’ Compensation insurance claims. Our model does not explicitly recognize an offset for health insurers from a shift to Workers’ Compensation claims.

For employers with self-insured Workers’ Compensation programs, one catastrophic risk is the possibility that a COVID-19 claim could turn into a long-term ESRD claim with lifetime medical costs that can easily be in the millions of dollars. Typically, these patients, even when in an employer plan are Medicare-eligible. Employers should consider their obligations to establish a Workers Compensation Medicare Set-Aside Arrangement to indemnify Medicare for the medical costs they pay resulting from workplace diseases or accidents.

Summary

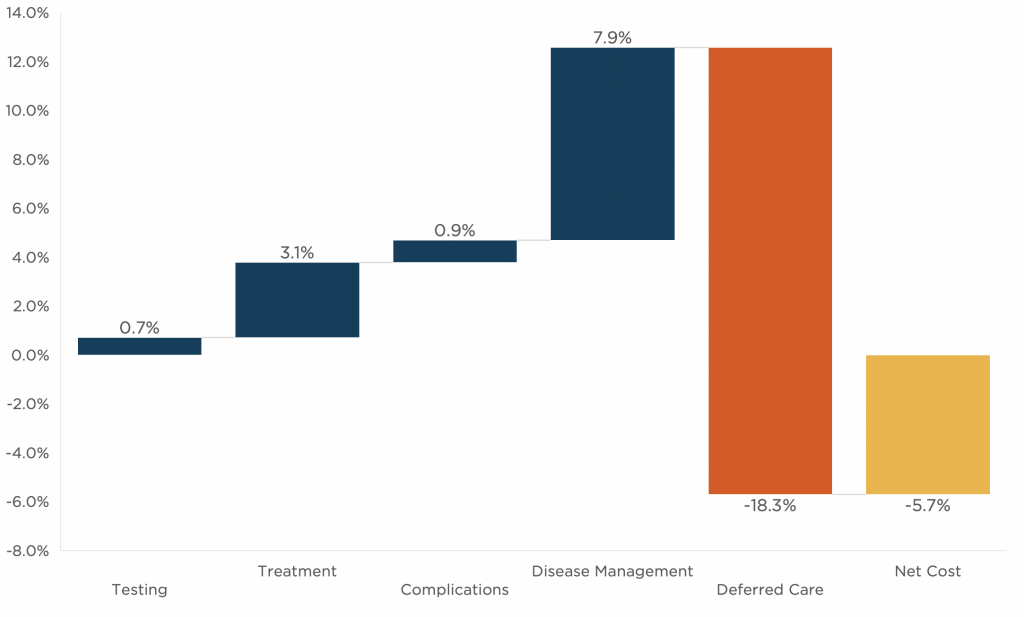

As of the date of this publication, our model calculates net decrease in healthcare spending of $135B in 2020 and an increase of $36B in 2021 as a result of all impacts of COVID-19. In this context payers include all private health plans, self-insured employers, Medicare, Medicaid, and CHIP populations, and their stop-loss reinsurers. These beneficiaries total approximately 90% of the U.S. population. Excluded from these costs are changes in the level of cost-sharing by beneficiaries.

2020 Net Cost of COVID-19

Source: EPIC Modeling

The net costs of the impact of COVID vs. the status quo fall disproportionately on stop-loss insurers, and Medicare populations may even have a net negative cost of care in 2020.

2020 Cost of COVID-19 by Population

Commercial | Medicare | Medicaid |

|

|---|---|---|---|

| Population Size | 176,700,000 | 44,000,000 | 70,700,000 |

| Infection Rate | 14.0% | 16.0% | 11.0% |

| % Symptomatic (of Infection) | 4.1% | 4.8% | 3.5% |

| COVID-19 Testing | |||

| Percent of Population Tested | 15% | 15% | 15% |

| Number of Tests Performed | 26,505,000 | 6,600,000 | 10,605,000 |

| Cost per Test | 240 | 100 | 100 |

| Testing Cost | 6,400,000,000 | 700,000,000 | 1,100,000,000 |

| COVID-19 Treatment | |||

| % Hospitalized | 5.0% | 21.1% | 4.8% |

| Non-ICU | 4.4% | 11.5% | 3.7% |

| ICU w/o Ventilator | 0.1% | 1.8% | 0.2% |

| ICU w/ Ventilator | 0.5% | 7.7% | 0.8% |

| Number Hospitalized | 364,886 | 445,368 | 119,695 |

| Non-ICU | 318,413 | 243,276 | 92,829 |

| ICU w/o Ventilator | 9,895 | 38,940 | 6,222 |

| ICU w/ Ventilator | 36,577 | 163,152 | 20,644 |

| Average Length of Hospital Stay | |||

| Non-ICU | 12 | 12 | 12 |

| ICU | 18.5 | 18.5 | 18.5 |

| Cost per Day | |||

| Non-ICU | 3,000 | 1,250 | 2,250 |

| ICU w/o Ventilator | 8,250 | 3,440 | 6,190 |

| ICU w/ Ventilator | 8,810 | 3,670 | 6,600 |

| Cost of COVID-19 Treatment | 18,900,000,000 | 17,200,000,000 | 5,700,000,000 |

| Complication Related to COVID-19 | |||

| ECMO | 100,000,000 | 100,000,000 | 0 |

| Infections | 1,200,000,000 | 1,300,000,000 | 400,000,000 |

| Heart Disease | 1,300,000,000 | 1,000,000,000 | 200,000,000 |

| Kidney Disease | 3,300,000,000 | 2,600,000,000 | 600,000,000 |

| Cost of COVID-19 Related Complications | 5,900,000,000 | 5,000,000,000 | 1,200,000,000 |

| Deferred Care | |||

| Net Savings from Deferred Services | -146,200,000,000 | -48,300,000,000 | -41,700,000,000 |

| Returned Services w. Complications | 22,200,000,000 | 7,200,000,000 | 9,900,000,000 |

| Cost of Deferred Care | -124,200,000,000 | -41,100,000,000 | -31,800,000,000 |

Total Cost | -93,000,000,000 | -18,200,000,000 | -23,800,000,000 |

Our estimates are highly subject to an understanding of the overall spread of infection in the United States during 2020 and 2021. Our model considers many different scenarios, whose average mortality directly due to the virus is about 300,000 lives before the end of 2021.

| Year | Commercial | Medicare | Medicaid | Total |

|---|---|---|---|---|

| 2020 | -17.3% | -15.2% | 4.9% | -15.5% |

| 2021 | 2.4% | 9.8% | -5.7% | 4.2% |

This summary of our model is a good guide for self-insured employers to consider in setting claims reserves and budgeting retained claims costs. Please approach your EPIC broker for a projection specific to your employee demographics, geography, self-insured retention, effective date, and level of social distancing.